[Generated with Gemini]

Every May, I attend the organized by Mauldin Economics, whose work I have been following for years, and find them data-driven and level-headed. For five days, I listened to a few dozen accomplished, award-winning economists, financial analysts, money managers, entrepreneurs, venture capitalists, political and geopolitical analysts, and professors present their research and views on the US economy, financial markets, global markets, and geopolitics. I’ve found it extremely valuable and helpful in helping myself better understand the general condition and the trend of the US economy and monetary policy environment (i.e. interest rate), which I strongly believe should shape any investor’s view on constructing or adjusting their portfolios, be it real estate, stocks, or bonds. So, if you are interested in in-depth analysis of the US economy, the financial markets, or geopolitics, I highly recommend attending this conference each year.

In this week’s article, I will attempt to summarize what I learned about the inflation expectations from these presenters this year. Note that I’m not an economist or financial analyst; these are strictly my own personal understandings from the presentations.

Higher Inflation for Longer

The argument for higher inflation for longer is based on two reasons.

The first is the oil price shock. This has been all over the headlines. Higher oil prices translate into higher energy, transportation, and production costs and therefore put significant inflationary pressure on goods and services.

Will the oil price drop back to pre-Iran War levels when the Strait of Hormuz is eventually reopened? No one knows. The global oil supply and demand structure could have been altered by the war.

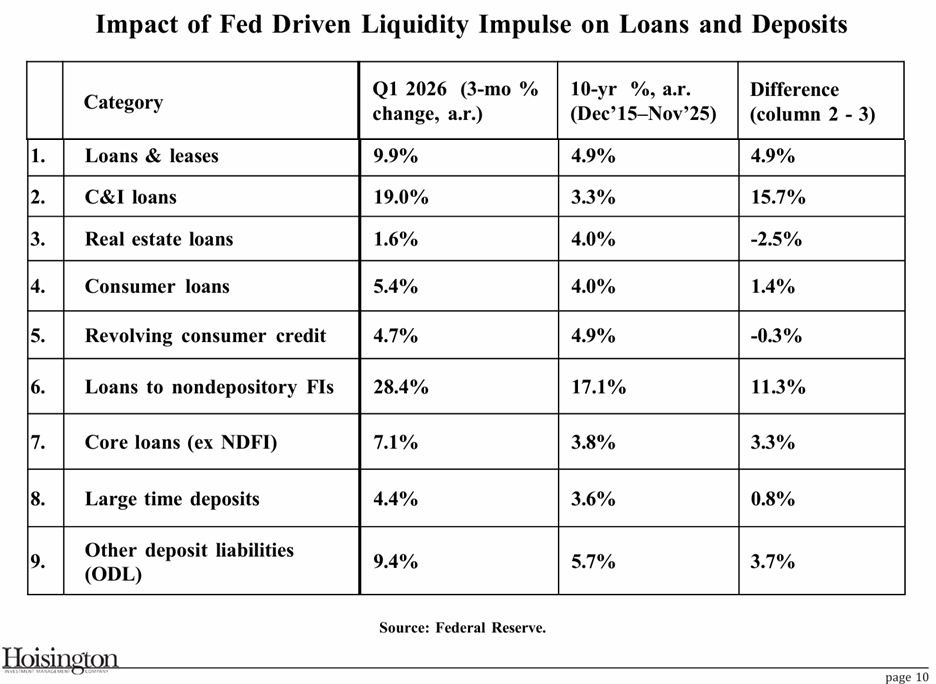

The second reason is the Fed’s liquidity impulse. Starting in mid-December, the Fed began purchasing roughly $40 billion a month in Treasury bills, lifting holdings from just under $200 billion to nearly $430 billion by late April!

[]

Normally, that expansion would appear on the Fed’s balance sheet. But this time, the money that flowed directly into bank balance sheets (after the Fed purchased the Treasury Bills) was put to work. Loans and leases grew at nearly a 10% annualized rate, while commercial and industrial lending was running closer to 20%. In other words, the liquidity injected by the Fed “became hot money that got multiplied throughout the system, expanding the money supply and triggering inflation not just in the first quarter but in future quarters as well.”

I did not see this one coming, but the analysis makes sense.

But what about a possible recession?

Another analyst argued that the bigger danger is recession, not inflation.

Historically, oil price shocks have been associated with recessions and bear markets. So, a recession could follow this round (of the oil price shock).

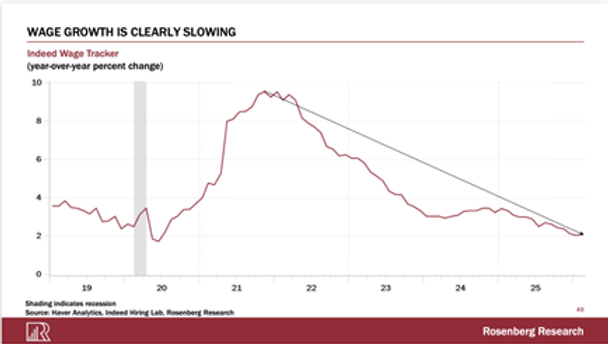

The softening labor market may also put the brakes on inflation. Unemployment expectations are already at recessionary levels. Stalling wage growth does not provide the fuel to chase prices higher.

The BLS (Bureau of Labor Statistics) initially reported 1.7 million jobs created in 2025. After revisions and quarterly census adjustments, that number fell to just 123,000. More importantly, beneath the headline numbers, the private sector posted net job losses in both the second and third quarters of the year.

Consumer data is also deteriorating: a record-low flat real retail sales, a depleted savings rate, etc.

A recession means less demand and downward pressure on prices (inflation).

Concluding Thoughts

My take is that it is a safer bet on higher inflation for longer. The drivers of higher inflation are already at work (an oil price shock and an increased money supply), while a recession has not been confirmed. Plus, stagflation happened before (when the economy was stagnant but the inflation was high), and could happen again if the conditions arise.

I would expect average inflation in the mid-3% range over the next few years, or even longer, given the current trend of deglobalization and the emphasis on national economic resilience over cost efficiency.

Maintaining realistic expectations about inflation is critical for any investor, as the inflation rate is the baseline rate of return (over your projected hold period) that you HAVE to achieve just to stay your ground. It does not matter whether you invest in real estate, stocks, or bonds; you must beat inflation if you want to maintain the purchasing power (therefore, your living standard) of your money. And that requirement is much higher now than in the pre-COVID, low-inflation environment.

For long-term real estate investors, rental income must continue rising faster than operating costs and consumer inflation over decades of ownership. Properties located in markets with sustained population growth and constrained housing supply have historically performed better in inflationary environments than those in stagnant markets.

…Cleo