Home values fell sharply in Las Vegas, but in the rental segment we targeted, rents remained stable. This case study shows why tenant selection mattered more than headlines.

Las Vegas was one of the hardest-hit housing markets during the 2008 financial crisis. Home values fell sharply. Many owners lost equity, faced payment pressure, and were forced to sell or go into foreclosure.

But property values and rental income are not the same thing.

That distinction matters. Investors do not lose properties because values fall on paper. They lose properties when the income does not cover the expenses long enough to survive the downturn.

This case study looks at one of the primary rental areas we targeted in Las Vegas. We studied a specific property profile: 3+ bedrooms, 2+ car garage, 1,200 to 1,500 square feet, one or two stories, and no private pools.

Study Area and Property Profile

The map below shows the primary rental area used for this study. We then looked at conforming properties within that area that matched the profile above.

This matters because broad market averages often hide what is really happening in the segment investors actually buy.

What Happened to Property Prices

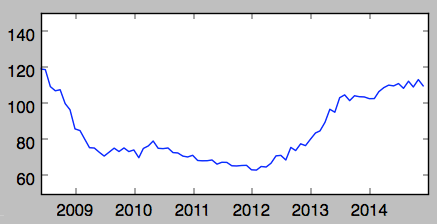

The first chart shows the average monthly sale price per square foot for conforming properties in the selected area from 2008 to 2014.

During the 2008 crash, these properties were selling for about $120 per square foot. By 2012, the average had fallen to about $70 per square foot.

That was a major drop in value.

For many owners, a drop like that created real pressure. If they had weak tenants, poor cash reserves, or properties that did not produce reliable rent, they were exposed. A sharp fall in value can be survived. A loss of income usually cannot.

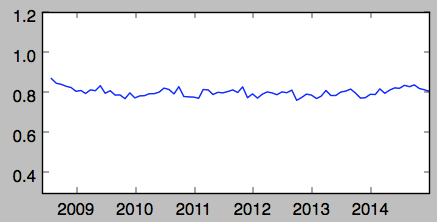

What Happened to Rents

The second chart shows rental rates per square foot for similar properties in the same area over the same period.

While sale prices dropped sharply, rents changed very little.

That is the key result.

The asset value fell. The income stream did not.

That put owners of well-selected rental properties in a very different position from owners who depended on appreciation, resale, or unstable tenant segments. If rent remained steady and the property stayed occupied, the investor could continue through the downturn without being forced to sell.

Why Our Clients’ Income Held Up

Before the crash, in 2005 and 2006, we spent a great deal of time studying tenant behavior.

We were not asking, “What property looks like a good deal today?”

We were asking a different question:

Which tenant segment is most likely to stay for many years, pay rent on time, and take care of the property, even during a difficult market?

That research led us toward a tenant profile with several important characteristics:

- Families with children, who tend to stay longer

- Households with stable, credit-dependent financial lives

- Tenants in roles that are often more recession-resistant, including business-critical, income-producing, and government-related jobs

- Renters looking for practical single-family homes that fit long-term household needs

Then we bought properties that fit what those tenants actually wanted to rent.

That was the key. We did not just identify a stronger tenant segment. We matched that segment with the right housing product.

The Real Lesson From 2008

The lesson from 2008 is not that real estate prices never fall. They do.

The lesson is that income stability depends on tenant quality and property fit, not just market appreciation.

A property can lose a large amount of market value and still perform as a rental if tenant demand remains strong and the income continues. On the other hand, a property can look attractive on paper and still fail if it serves the wrong tenant segment.

That is why we start with the tenant, not the property.

Final Takeaway

During the 2008 financial crisis, property prices in this Las Vegas rental segment fell sharply. But rents remained stable.

That stability was not an accident.

It came from selecting a tenant segment with more reliable behavior and buying properties that fit that segment well.

Many investors focus first on price, projected appreciation, or headline cash flow. We believe the better place to start is with the income stream. And since tenants produce the income, the first question should always be:

Who is most likely to keep paying the rent, even when the market gets hard?

Want to invest for stable long-term income, not just short-term appreciation? Review our investment framework or schedule a call to discuss your goals.