Most investors ask this question when a property no longer feels simple. Maybe cash flow is lower than expected. Maybe the property has appreciated and has significant equity. Maybe maintenance, taxes, insurance, regulations, or vacancy have started to eat into returns. The decision process can feel complex, but the right answer depends on one question: Does this property still support your long-term financial goals?

The best indicator is whether rents and prices have outpaced inflation over the past 5 to 7 years, and if they are likely to continue to do so into the foreseeable future.

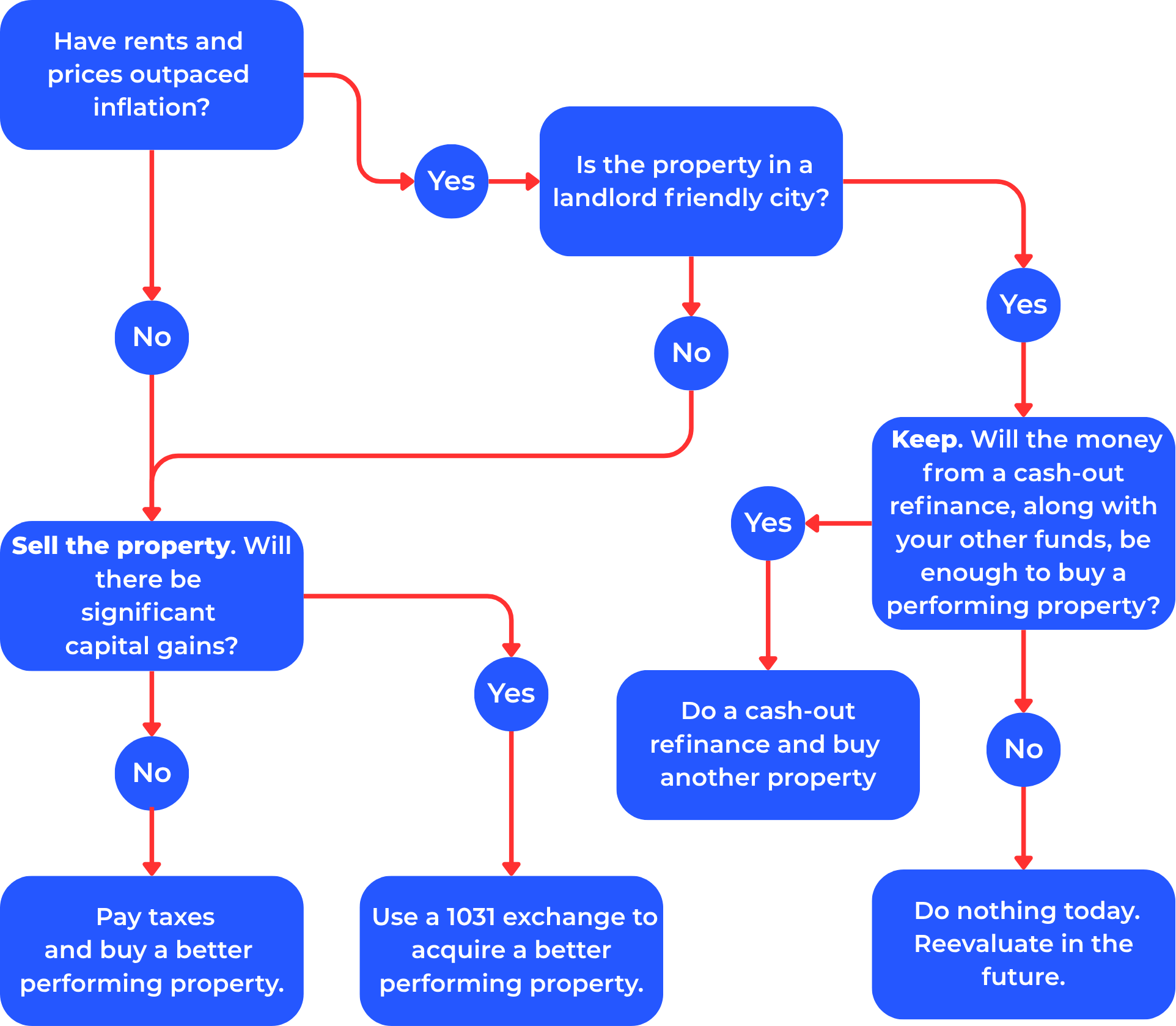

I created a decision tree to simplify the decision, as shown below.

Focus on net rent, not gross rent

What matters is how much income remains after all costs. Some of the major costs are shown below.

Taxes and Insurance

Taxes and Insurance costs vary widely by city. Below is a comparison for a $400,000 property.

| State | Average Insurance | Property Tax Rate | Annual Property Tax | Total |

|---|---|---|---|---|

| Florida | $10,996 | 0.91% | $3,640 | $14,636 |

| Texas | $2,317 | 1.68% | $6,720 | $9,037 |

| Nevada | $965 | 0.59% | $2,360 | $3,325 |

Sources:

- State average property tax.

- Average insurance cost, except for Florida.

- Florida’s average insurance cost.

Compared to Nevada, these higher-cost states require more cash flow to compensate for higher taxes and insurance.

- A Florida property needs to generate about $11,311 more cash flow per year, or $943 per month, to compensate for the higher taxes and insurance.

- A Texas property needs to generate about $5,712 more per year, or $476 per month, to compensate for the higher taxes and insurance.

Vacancy Cost

Vacancy cost is what you spend between tenants. It depends on:

- Length of stay: The longer a tenant stays, the lower your vacancy cost over time.

- Time to re-rent: Some properties rent in days, others take months.

- Monthly carrying costs: These include mortgage payments, taxes, insurance, utilities, and maintenance.

- Property manager skill: Selecting reliable tenants has a major impact on vacancy cost. Few property managers have the skill to consistently select reliable tenants.

- Turnover costs and time: The time and costs to make the property rent-ready again depend on tenant behavior and the property manager’s tenant-selection skills. Some tenant groups cause more damage than others.

If vacancy costs are high, your actual income will fall short of expectations.

Rent Control

Rent control can act like a hidden tax. It may limit rent increases, restrict tenant selection, and make evictions difficult. These limits can cost more than taxes or insurance. Always check local regulations before investing. To determine if there are rent controls in a given city, Google or AI search for something similar to “Does [city] have rental regulations?”

Maintenance Cost

Maintenance costs can turn a profitable property on paper into a financial loss. Maintenance costs are a function of:

- Property condition: Properties with deferred maintenance will have higher ongoing costs.

- Property age: Older properties often have aging systems, which increase the need for repairs and replacements.

- Climate: Moisture, freezing temperatures, and snow increase maintenance costs.

- Construction materials: Some materials cost less to maintain. For example, stucco siding typically requires less maintenance than wood siding.

- Tenant segment: Some tenant groups take better care of the property than others.

The Bottom Line

The decision to sell, refinance, complete a 1031 exchange, or hold a property depends on one thing: Does the property support your financial goals?

Evaluate rent growth, appreciation, and all costs. Then decide based on long-term performance, not short-term metrics.

If you are deciding whether to sell, refinance, exchange, or hold an investment property, the first step is not the transaction. The first step is understanding whether the property still fits your long-term financial goals. If you would like help thinking through that decision, you can schedule a strategy call with our team.