Over the past 16 years, I’ve worked with nearly 200 first-time investors. From my experience, until they go through our training, most are completely focused on ROI and cash flow. I will offer some essential tips for first-time investors in this article.

- You’re not buying real estate. You’re buying a lifelong income stream.

- Vacancy costs can be a killer so knowing how to estimate vacancy costs is critical.

- ROI and cash flow only predict a property’s performance under ideal conditions on the first day of a lifetime hold. They tell nothing about future performance.

- “You can only count on today.”

You Are Not Buying Real Estate

Yes, the result will be purchasing a property, but that is not what you are buying. You are buying an income stream. You are buying a method of permanently getting off the daily work treadmill and living on your terms. So, what matters is not the property itself; it is the income that the property produces.

The net rental income is called cash flow. The formula for cash flow is:

- Cash Flow = Income – Expenses

To make money, your income must be greater than your expenses. The income, or rent, is what I will focus on in the remainder of the article.

Probable, Not Gross, Income Is What Matters

Many people calculate annual income as 12 times the monthly rent. If a performing tenant always occupied the property, this would be true. However, reality is far different. A more realistic view of annual income is:

- Annual Income = 12 x Monthly Rent – Vacancy Cost – Expenses

I will ignore expenses and only focus on vacancy costs.

There is no way to know precisely your future vacancy costs. However, you can estimate the average future vacancy cost based on the tenant segment your property attracts and their historical behaviors. You can obtain such historical information by interviewing property managers. I will use my tenant segment research in Las Vegas to show you how to estimate vacancy costs.

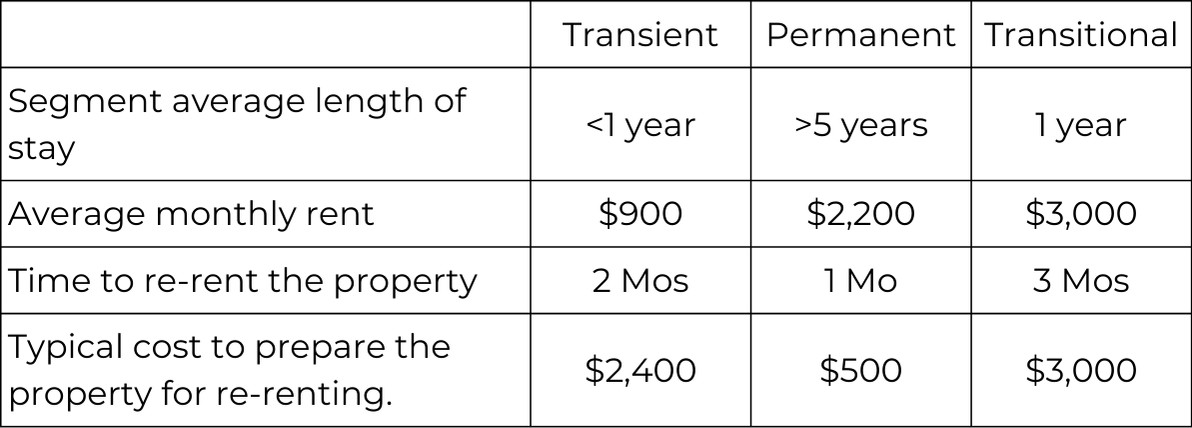

Las Vegas has three primary tenant segments: Transient, Permanent, and Transitional. Each segment is named based on the average length of stay. Below is a table showing the average stay, average rent, and additional information I will use to estimate the average annual vacancy cost for each of the three segments.

Although the actual cost calculation for a property is more complex due to property-specific carrying costs, the following example will help illustrate the concept. For simplicity, I will assume the monthly recurring cost (debt service, taxes, insurance, utilities, etc.) for properties across all three segments is $2,500/Mo.

The formula for vacancy cost is:

- Vacancy Cost = Months to Rent x Carrying Costs + Renovation Cost

Calculating the per vacancy cost for the three segments:

- Transient: 2 x $2,500 + $2,400 = $7,400

- Permanent: 1 x $2500 + $500 = $3,000

- Transitional: 3 x $2,500 + $3,000 = $10,500

To convert the per vacancy cost into an annual vacancy cost, divide the per vacancy cost by the average length of stay for each segment.

- Annual Average Transient Vacancy Cost: $7,400 / 1 Yr = $7,400/Yr

- Annual Average Permanent Vacancy Cost: $3000/ 5 Yrs = $600/Yr

- Annual Average Transitional Vacancy Cost: $10,500 / 1 Yr = $10,500/Yr

Considering the cost of vacancy for each segment, we can now calculate the potential annual income for each of the three segments.

- Transient Probable Income: $900 x 12 – $7,400 = $3,400/Yr

- Permanent Probable Income: $2,200 x 12 – $600 = $25,800/Yr

- Transitional Probable Income: $3,000 x 12 – $10,500 = $25,500/Yr

Based on the above calculations, you can modify your cash flow calculations to use probable income and not gross income in your calculations as follows:

- Transient Cash Flow = Gross Income x $3,400/($900 x 12 ) – Expenses Or Gross Income x 31% – Expenses

- Permanent Cash Flow = Gross Income x $25,800/($2,200 x 12 ) – Expenses Or Gross Income x 98% – Expenses

- Transient Cash Flow = Gross Income x 25,500/($3,000 x 12 ) – Expenses Or Gross Income x 71% – Expenses

Even though a property might look like a cash cow based on gross rent, it could be a money pit when vacancy cost is included.

It’s important to note that vacancy cost is a function of carrying cost, time to rent, and turn cost. These factors depend on the property and the tenant segment it attracts. Contrary to popular belief, there is no relationship between vacancy cost and the rent amount.

The Limitations of ROI and Cash Flow

ROI and cash flow only estimate how a property will likely perform on day one under ideal conditions. They tell you nothing about day two onward. Because you will hold the property for many years, what happens after day one is far more important than day one.

For example, suppose you are choosing between two properties in different cities.

Property A:

- Price: $300,000

- Rent: $2,000/Mo

- Rent growth rate: 2%/Yr

Property B:

- Price: $300,000

- Rent: $1,500/Mo

- Rent growth rate: 8%/Yr

Based on the above data, it is a no-brainer that Property A is the better investment, right?

Now, let’s look beyond first-day performance.

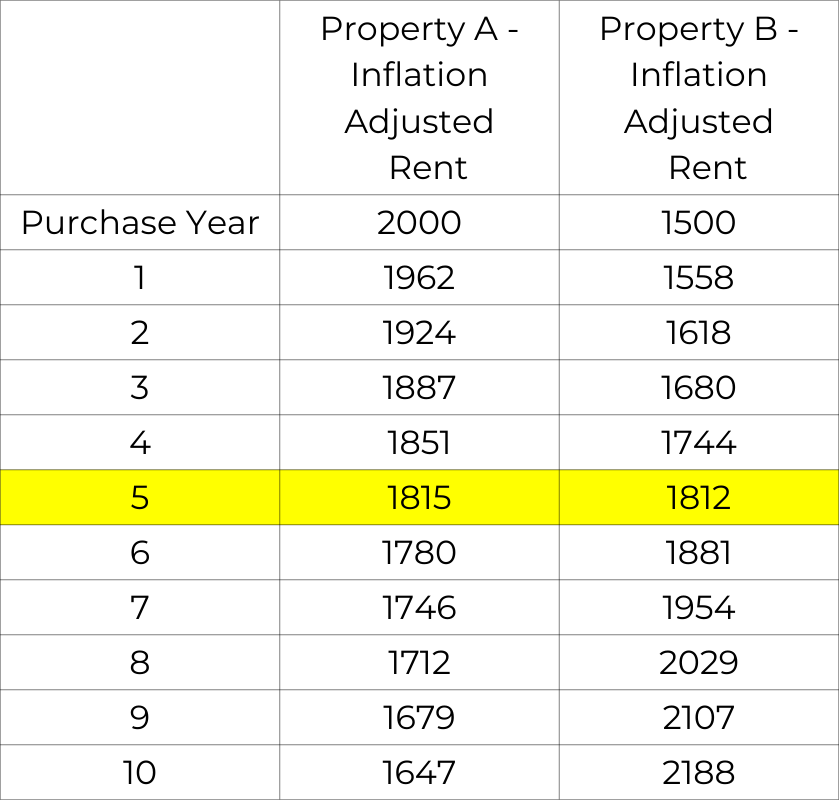

I will assume inflation is 4%/Yr. What will be the inflation-adjusted rent (or buying power) for both properties over the first ten years?

Because rents where Property A is located are not increasing as fast as inflation, your inflation-adjusted income declines every year. In comparison, because Property B’s rents are increasing faster than inflation, the inflation-adjusted income increases every year. By year 5, both properties have almost the same inflation-adjusted income. After year 5, Property B is the better long-term investment. Buying Property A would be a financial disaster if you plan on holding the property for over 5 years.

The lesson is that property evaluation based solely on day-one metrics such as cash flow and ROI can lead to bad decisions and losses in the long run.

“You Can Only Count on Today”

The most frequent justification I hear for making property selections based on day-one cash flow and ROI is, “You can only count on today.” However, this belief assumes that the world is static and that nothing will change. Change is the only constant in life, so this is an invalid assumption.

For example, if you purchase property in a city where rents have not kept pace with inflation, achieving financial freedom with these properties is impossible. This is because the amount of goods and services your rent can buy decreases every day due to inflation. This is shown in the above example of Property A and Property B.

The best analogy I know for rent growth and inflation is an escalator. Imagine watching someone attempting to walk up a descending escalator. The person walking up represents rent growth, and the downward-moving escalator represents inflation. If the person doesn’t walk up fast enough to outpace the escalator’s descent, they will move downward. So, even if rents increase, if inflation decreases faster, your buying power, or the actual value of your money, is declining.

Summary

In this post, I outlined important tips every real estate investor needs to consider. These tips are not just suggestions but integral parts of successful real estate investing. Ignoring or failing to consider these tips can have serious negative long-term financial consequences.